Research firm CoreLogic reported that there were 55,000 completed foreclosures nationally, down from 67,000 in September 2014, a 17.6% decrease. The report went on to say that there has been a 52.8% decline since the peak of the foreclosure problems when there were 117,438 foreclosures in September 2010. In addition, completed foreclosures jumped 49.5% from August 2015 to September 2015, which was due in part to the result of an annual public auctioning of thousands of tax-foreclosed properties in Wayne County, Michigan.

On the lighter side, with Thanksgiving right around the corner, here are a few facts: Approximately 46 million turkeys are eaten on Thanksgiving every year. The Macy’s Thanksgiving parade began in 1924 with only 400 employees. More alcohol is consumed on Thanksgiving than any other holiday of the year. One last fact, while Turkey does contain tryptophan, which could make us feel drowsy, sleepiness is more likely caused by the over-consumption of alcohol and food, especially desserts. So maybe skip the desserts if you want to stay awake for more family time.

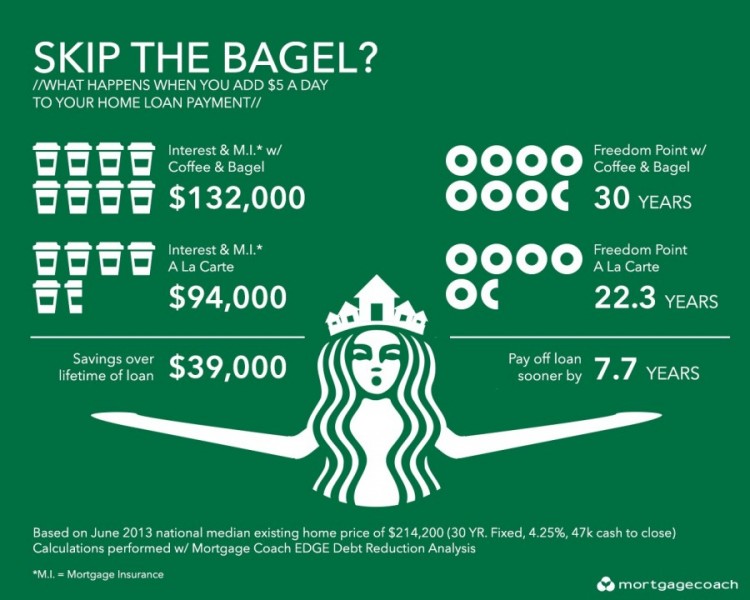

Speaking of skipping things, take a look at this infographic displaying the huge positive outcome that ‘skipping the bagel’ or daily designer coffee run can have. It’s always interesting to see how small changes can add up long-term, especially when it is as substantial as this!

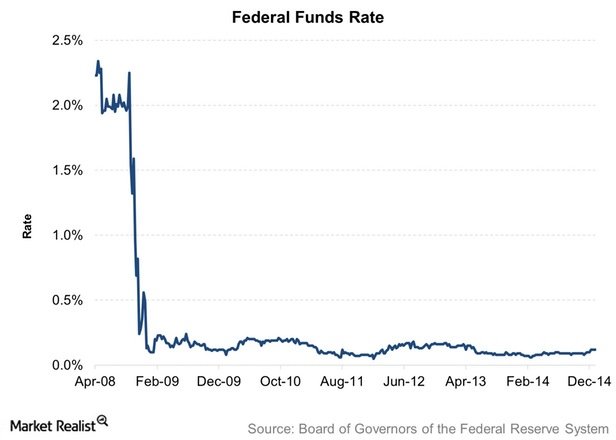

Getting back on track; the Federal Reserve almost set to raise interest rates (the Fed Funds Rate) next month, consumers could be impacted. If you are buying a home and using an adjustable rate mortgage (ARM) to finance the purchase, those rates will move higher, as ARMs closely follow the Fed Funds Rate. If you are shopping for a home equity loan, those rates will also increase, as will home equity lines of credit. Interest rates on most credit cards and rates on certificates of deposits, money markets, and savings accounts will increase as well.

The Labor Department reported on Friday that U.S. employers added 271,000 new workers in October, well above the 181,000 expected and up from the lower numbers seen in August and September. The report showed hiring across many sectors of the economy. The Unemployment Rate fell to 5 percent, the lowest level since April 2008, just before the Great Recession.

The strong number could push the Fed to raise interest Rates next month at the FOMC meeting.